The IDnow Blog: Ideas That Build Trust.

Explore expert commentary, practical perspectives and forward-looking ideas from across the world of identity verification, fraud prevention and compliance. From AI-powered attacks to regulatory reforms like eIDAS 2.0 and PSD3, the IDnow blog is your hub for understanding what’s happening and what’s next.

Latest Blogs.

Europe’s AML Rules are Being Rewritten. Here’s What the July 10 Deadline Means for You.

On July 10, 2026 the EU’s new Anti-Money Laundering Authority (AMLA) will submit the technical standards that will define compliant customer verification across Europe […]

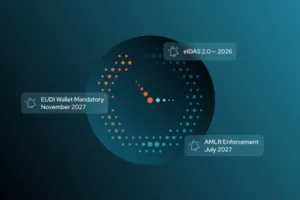

EU AMLR 2027: The Compliance Clock Is Ticking. Here’s What the Next 18 Months Mean for Your Identity Stack

AMLR lands in July 2027. Mandatory EUDI Wallet acceptance follows in November. Two deadlines. One fixed timetable. And an identity […]

“Simple on the surface, powerful underneath,” 0TO9 on Going First with IDnow’s Trust Platform.

When IDnow launched the Trust Platform – a single-integration infrastructure for identity verification, fraud prevention, biometric authentication, and qualified digital trust – […]

5 Questions For… the European Blockchain Sandbox Lead.

In the first instalment of IDnow’s ‘5 Questions For…’ interview series, we sit down with Marjolein Geus to discuss how the European […]

The Borders that Digital Trust Can’t Cross… and What it Will Take to Change That.

From post-quantum cryptography to cross-continental Digital Product Passports, the infrastructure of global digital trust is being built right now. Here’s what the frontlines look like. […]

KYC in 2026: The 4 Trends Already Changing the Game

IDnow’s Director of Product, Jonas Mendes, has spent years watching how financial institutions approach digital identity – and in 2026, the […]

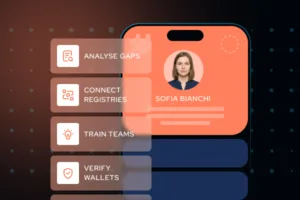

10 Steps that European Banks Must Take to Meet the EUDI Wallet Deadline.

European banks have until December 2027 to accept EUDI Wallets. Here’s everything they need to do to ensure they’re ready for the deadline. In the previous entry in our ‘Everything […]

EU Digital Identity & Compliance: What Happened in April 2026

Behind the billions stolen by fraud lies a dark reality: hundreds of thousands of human trafficking victims, enslaved to carry out scams. This article explores how criminal networks recruit and train their forced workforce, and reveals the strategies banks can adopt, from enhanced identity verification to intelligence sharing, to break this cycle and protect their customers.

European Digital Identity Wallet Readiness: A Country-by-Country Assessment.

Which EU member states are ready for European Digital Identity Wallets? Not all will make the December 2026 deadline. Find out how your country […]

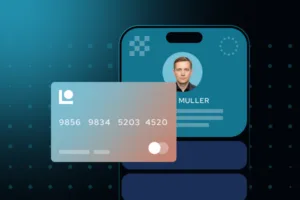

The EUDI Wallet Explained: Everything Banks Need to Know Before 2027.

In the first of our three-part ‘Everything You Need to Know About the EUDI Wallet’ blog series, we explain what the EUDI Wallet is, what data it contains, and why the […]

From KYC to TYC: What Changes and Why it Matters.

In the previous article ‘Why KYC Is No Longer Enough?’, we argued that traditional KYC, however well-executed, is structurally limited […]

Why KYC Is No Longer Enough: The Identity Verification Wake-Up Call

For years, the identity verification playbook followed a reassuringly simple script. A customer applies for an account. Documents are checked. A face is matched. A sanctions list is screened. A Know Your Customer (KYC) process is completed. Done. In a more predictable era, this was enough. Identity was treated as a fixed attribute; something verified once, filed away, and assumed to remain true indefinitely. The onboarding check was both the starting gate and […]

Most Popular Blogs.

-

18+ only? Age verification for adult content.

-

Buying crypto without a KYC check? Here’s why it’s risky for users and platform operators.

-

Online gambling in Germany: Regulations, restrictions, and ramifications.

-

Cryptocurrency in Germany: Is it regulated and safe?

-

Everything you need to know about getting a UK gambling license.