The IDnow Blog: Ideas That Build Trust.

Explore expert commentary, practical perspectives and forward-looking ideas from across the world of identity verification, fraud prevention and compliance. From AI-powered attacks to regulatory reforms like eIDAS 2.0 and PSD3, the IDnow blog is your hub for understanding what’s happening and what’s next.

Latest Blogs.

The true face of fraud #5: The digital heist, or how billions of scam money get laundered

Modern financial crime operates as two tightly coupled systems: fraud, which extracts money from victims, and money laundering, which moves and disguises […]

The Identity Check is Dead. Long Live the Identity Relationship.

The way businesses verify who their customers are is about to fundamentally change. Here’s what that means, and why identity relationships are so important. Key […]

The True Face of Fraud #4: 5 Reasons Why the Industry Is Losing the War on Fraud

We think we understand fraud. We study it, legislate against it, invest billions fighting it. And yet losses keep climbing, […]

PSD3 News for Financial Services: 5 Critical Changes Every PSP Must Act On Now.

The EU is replacing the Payment Services Directive 2 (PSD2) with a new two-part framework. Here’s what’s changing, why it matters, and what financial services firms need […]

Lessons From… Building a Platform That Makes Compliance Simple Again.

Jonas Mendes, Director of Product for the IDnow Trust Platform, explains the thinking behind the Platform’s Orchestrate, Observe, Decide capabilities, and why the […]

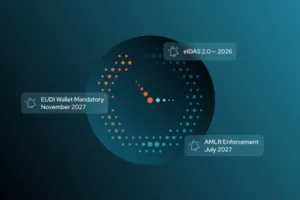

Europe’s AML Rules are Being Rewritten. Here’s What the July 10 Deadline Means for You.

On July 10, 2026 the EU’s new Anti-Money Laundering Authority (AMLA) will submit the technical standards that will define compliant customer verification across Europe […]

EU AMLR 2027: The Compliance Clock Is Ticking. Here’s What the Next 18 Months Mean for Your Identity Stack

AMLR lands in July 2027. Mandatory EUDI Wallet acceptance follows in November. Two deadlines. One fixed timetable. And an identity […]

“Simple on the surface, powerful underneath,” 0TO9 on Going First with IDnow’s Trust Platform.

When IDnow launched the Trust Platform – a single-integration infrastructure for identity verification, fraud prevention, biometric authentication, and qualified digital trust – […]

5 Questions For… the European Blockchain Sandbox Lead.

In the first instalment of IDnow’s ‘5 Questions For…’ interview series, we sit down with Marjolein Geus to discuss how the European […]

The Borders that Digital Trust Can’t Cross… and What it Will Take to Change That.

From post-quantum cryptography to cross-continental Digital Product Passports, the infrastructure of global digital trust is being built right now. Here’s what the frontlines look like. […]

KYC in 2026: The 4 Trends Already Changing the Game

IDnow’s Director of Product, Jonas Mendes, has spent years watching how financial institutions approach digital identity – and in 2026, the […]

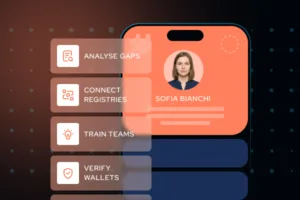

10 Steps that European Banks Must Take to Meet the EUDI Wallet Deadline.

European banks have until December 2027 to accept EUDI Wallets. Here’s everything they need to do to ensure they’re ready for the deadline. In the previous entry in our ‘Everything […]

Most Popular Blogs.

-

18+ only? Age verification for adult content.

-

Online gambling in Germany: Regulations, restrictions, and ramifications.

-

Cryptocurrency in Germany: Is it regulated and safe?

-

Everything you need to know about getting a UK gambling license.

-

Buying crypto without a KYC check? Here’s why it’s risky for users and platform operators.